Happy Monday. This is Electric Avenue. The only e-Mobility newsletter that gives you the same feeling as waking up to Saturday morning cartoons as a kid. Your parents are still asleep, grab a 🥣 of cereal and tune in 📺.

Here’s what we have for you today:

Quick housekeeping 🏠

Why MSPs must adapt to survive ⚡

3 Links 🔗

Meme of the week 🤡

Let's get into it!

Quick housekeeping 🏠

ICYMI: Last week we celebrated our very 1st birthday at Electric Avenue. To celebrate, we’re having a 2x $50 (or EUR) Amazon gift card giveaway and launched this quick reader survey.

If you have two minutes to spare, we’d be very grateful if you take the survey. Make sure to enter your email at the end of the form (question #9.), if you’d like to participate in the giveaway.

And now back to regular programming. This week we have a thought-provoking guest post by our friend Michael Clarke on the future of e-mobility service providers (MSPs).

MSPs must adapt to survive⚡

The following is a guest post by Michael Clarke who holds experience at Telsa, Porsche, and Nio building charging services for EU customers. This post outlines the personal opinions and thoughts of Michael and does not necessarily reflect the opinions and views of his employers or Electric Avenue.

The role of the Mobility Service Provider (MSP) will change considerably over the next few years. Many will not survive the transition. This analysis is based on the assumptions and developments listed below.

Charging Point Operators (CPOs) are required to install credit card readers on all DC chargers and offer easy credit card payment on AC chargers. (read more about Card payment mandates @ public charging stations )

CPOs can earn higher margins when EV drivers pay directly, compared to the reduced rates offered to Mobility Service Providers (MSPs). Offering Autocharge through the CPO’s own app and cutting out the middleman will seem like an attractive option.

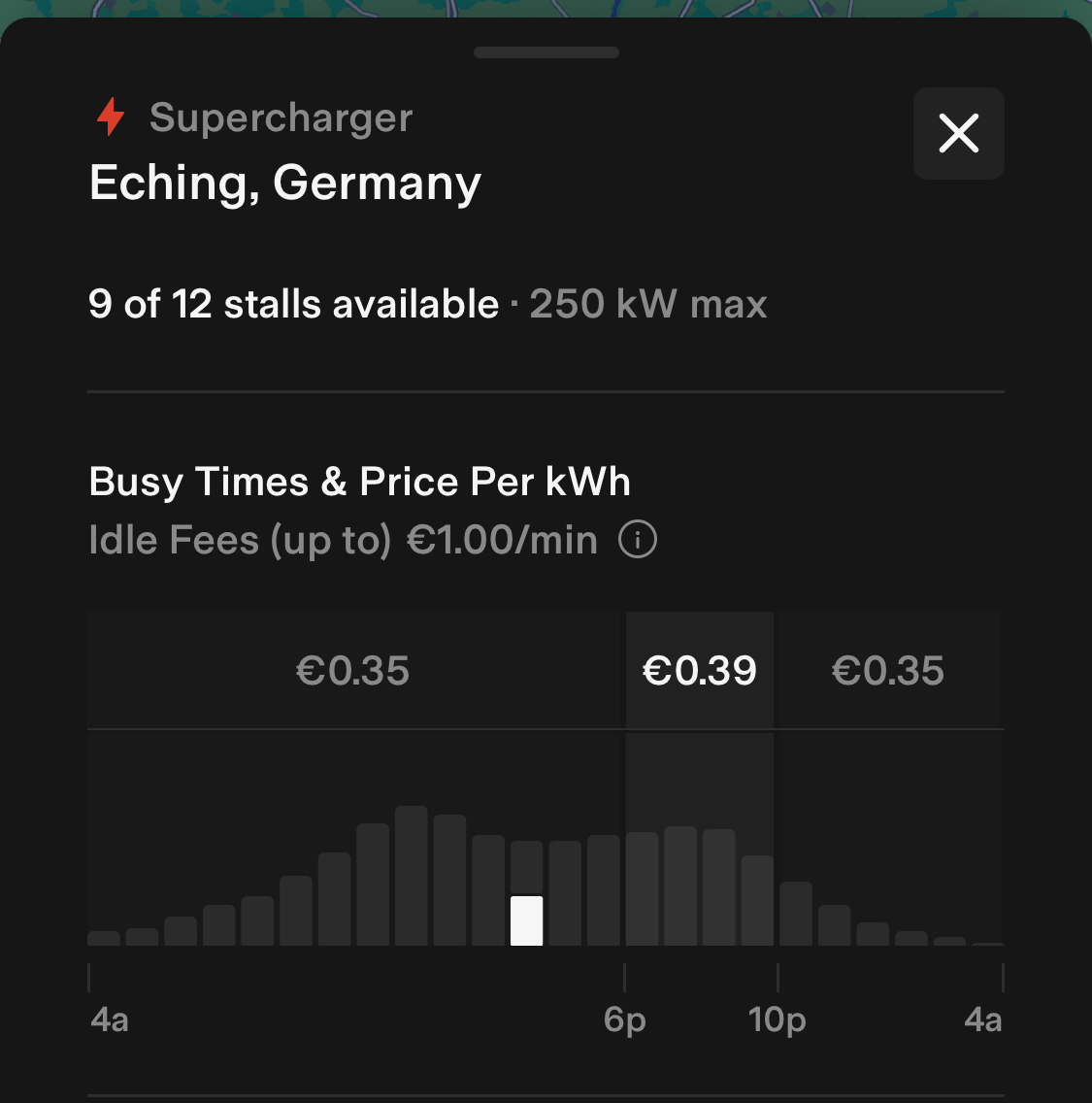

Available charging infrastructure will become a bottleneck in peak times, resulting in queues that EV drivers hate. Hence, CPO's (B2B) prices will become volatile to steer the demand with on-/off-peak prices (see Tesla’s pricing) and seasonal prices in/de-creases (e.g. holiday season).

Time of Use Tariff at Tesla Supercharger (Germany)

MSPs may struggle to pass on dynamic pricing to EV drivers due to technical complexities, leading to increased cherry-picking behavior among drivers, who will choose the credit card in low price times and the fixed MSP price in high price ad hoc times (see challenges to adopt site-specific pricing today).

Car manufacturers (OEMs), especially in the premium segment, will likely stop subsidizing MSPs, realizing that customers are content with paying via credit card without OEM incentives.

The convenience of ISO 15118 Plug & Charge will not be enough to entrench MSPs in the charging ecosystem due to its slowness, price transparency regulations, interoperability issues, and high maintenance effort.

MSPs may face financial challenges resulting in industry consolidation, leaving only a few MSPs operating across the EU.

The remaining MSPs will focus on B2B fleet solutions until VISA and Mastercard recognize the potential savings for fleet managers using debit cards restricted to charging.

Despite ongoing challenges with poor Point of Interest (POI) data quality, Google and Apple maps are poised to become the dominant databases of charging points.

The full story:

The charging ecosystem in Europe, including the UK, is undergoing significant changes due to the implementation of the Alternative Fuels Infrastructure Regulation (AFIR). According to AFIR, all DC fast chargers must be equipped with credit card readers. Additionally, AC chargers must be upgraded to support dynamic QR codes for credit card payments.

However, incorporating credit card terminals entails a substantial initial investment cost of around €300 per terminal, along with ongoing operational expenses, approximately 2.5% of each transaction plus a monthly fee. To justify this investment, Charging Point Operators (CPOs) will aim to encourage their customers to utilize credit card payments. To incentivize customers, CPOs will prioritize payment options based on their margin and profitability, with the following order from most to least financially beneficial:

Direct payment through the CPO's app using Single Euro Payments Area (SEPA) direct debit.

Credit card payment.

Third-party Mobility Service Providers (MSPs).

Consequently, CPOs will seek to strengthen their direct customer relationships and cut out the middleman by adjusting pricing mechanisms to make direct payment the most cost-effective choice. They will offer options such as monthly subscriptions within their app, providing even lower prices and the added convenience of Autocharge. Currently, EV drivers often need to choose the cheapest MSP RFID card for each charging session, a cumbersome practice for all parties involved - leading to the creation of services like Chargeprice. As a result, using an MSP is likely to become the most expensive option for EV drivers to pay. Surprisingly, MSPs were not able to lobby together and fight the, to them very dangerous, credit card payment mandates. Either because of fierce competition among them or because organizations like Chargeup Europe and CharIn represent CPOs primarily.

It is interesting to note that the United States, which is more credit card-friendly, does not have similar credit card reader requirements outside of California. However, for funding under NEVI, it will be mandatory to offer ISO 15118 Plug&Charge, a positive development for the nonexistent MSPs in America.

Editor’s note: Memes by Electric Avenue

As EV sales surge at a faster rate than anticipated, the public charging infrastructure faces the challenge of being overloaded, especially during peak travel times. Unfortunately, this situation is exacerbated by many Charging Point Operators (CPOs) opting to build numerous small charging sites instead of larger, more efficient charging hubs, ignoring the lessons learned from waiting cue theory.

The resulting waiting queues at these charging sites are affecting customers' willingness to pay for a kilowatt-hour (kWh) of energy. During high-demand periods, customers are more willing to pay a premium, while during quieter times, their willingness to pay decreases. Recognizing this dynamic, CPOs have the opportunity to adapt their pricing strategy based on customers' willingness to pay. Implementing such a pricing approach not only boosts revenue and utilization rates but also enhances customer satisfaction by spreading out demand and minimizing waiting times. Even today, it does not make sense that the price of a highly attractive (and expensive) HPC city location is the same from the same CPO as an abandoned 50 kW charger that is never used.

Generally, the market will see lower costs in summer when energy production from renewable sources is high and vice versa in winter. Therefore, CPOs must learn to control energy procurement and forward costs in- and decrease to their retail prices (independent if EV drivers pay directly or through EMPs). Trying to ignore this trend will only lead to bad compromises.

In contrast, CPOs that fail to adopt this customer-centric pricing mechanism may experience lower utilization rates, reduced margins, and decreased revenue, ultimately struggling to survive in the highly competitive charging business. Even today, CPOs need to compete on a local level with the charger next door. A single price per country reduces this flexibility. The current Tesla pricing model addresses these challenges effectively. By introducing one or two site-specific peak periods lasting several hours, with differentiated pricing tiers for weekdays and weekends, Tesla has achieved a balanced and viable long-term solution for CPOs.

In this pricing strategy, demand dictates the price rather than being tied to dynamic and ever-changing electricity prices based on day-ahead forecasts. Although directly affecting the cost of electricity to the CPO, it is unlikely that passing on these dynamic electricity costs to the user and having daily changing prices will enjoy much customer approval.

The key question now lies in how Charging Point Operators (CPOs) and Mobility Service Providers (MSPs) will adapt to the variable pricing direct payment method. CPOs may consider offering MSPs the same variable pricing structure, possibly with a slight bulk discount. However, MSPs may face technical limitations in managing variable prices for each CPO and even individual charging stations, as the Open Charge Point Interface (OCPI) does not currently support such complexity. This can be seen in that MSPs even resist constant, but site specific pricing by CPOs. Moreover, fixed pricing across their entire network is a crucial Unique Selling Proposition (USP) that MSPs prefer to offer.

Should MSPs insist on a fixed price from CPOs, they may end up paying a significant premium. On the other hand, if they accept the variable pricing fee structure, they are left with the decision of whether to pass this cost directly to the EV driver or adopt a mixed pricing calculation, hoping that EV drivers will utilize chargers during low-price periods. This approach may lead to cherry-picking behavior by EV drivers, who may opt for direct payment during low-price periods and the MSP card during periods where the direct payment price exceeds the MSP's rate.

Editor’s note: Memes by Electric Avenue

Arguing that consumers will revolt against this shift to dynamic pricing will be difficult in the face of the dynamic gas prices at fuel stations across the world. Multiple, and even unannounced price changes per day are the rule and are fully accepted by all parties involved.

Currently, car manufacturers subsidize many MSPs by providing MSP cards included in the vehicle price, often with reduced pricing for the first year. The rationale behind this was to attract customers away from Internal Combustion Engine (ICE) vehicles by offering subsidized charging prices to make Electric Vehicle (EV) ownership more appealing. Additionally, OEMs receive important Point of Interest (POI) data about charging stations for EV route planning.

However, with the intensifying price war, it is unlikely that this loss-making practice will continue indefinitely. As the industry evolves, car manufacturers may reconsider these subsidies, particularly when cost considerations and market competitiveness become paramount.

ISO 15118 Plug&Charge assumes a crucial role in this context. If Plug&Charge emerges as the predominant method of authentication at charging stations, it could significantly enhance the role of MSPs within the charging ecosystem. However, the pursuit of a "Tesla-like" charging experience has led to an overengineered solution, designed by committee, resulting in slow adoption and slow authentication times, high costs, and ongoing interoperability challenges. Simply having Plug&Charge supported on both the charger and the vehicle does not guarantee seamless functionality, as it requires MSPs and Charging Point Operators (CPOs) to agree upon pricing for charging to commence. This issue may become more prevalent, particularly given the challenge of variable pricing mentioned earlier.

Furthermore, both Plug&Charge and RFID cards face the challenge of informing EV drivers about specific charging prices for each session. In response to price transparency rules, MSPs might be compelled to prioritize APP-initiated charging to display the current valid variable price. Autocharge, with its known security risks, and Plug&Charge are not direct competitors but rather represent different aspects in the broader competition for charging payment dominance. The success of MSP-centric Plug&Charge depends heavily on a well-functioning roaming network and Public Key Infrastructure, which today still needs to be tested excessively to function properly. On the other hand, the relevance of Autocharge as a CPO-centric solution could grow if CPOs gain a larger share of the payment market with direct payment. Either way, removing the MSP from the value chain also eliminates a potential source of charging errors. The finger-pointing between CPO, MSP, and OEM for failed charging sessions will have one less player.

Editor’s note: Memes by Electric Avenue

The developments mentioned above are likely to exert financial pressure on MSPs, leading to significant consolidation within the industry. It remains to be seen who will emerge as the acquirer of smaller players, with other MSPs being an obvious candidate. However, some CPOs might also consider acquiring an MSP as a quick means to gain talent and digital solutions for their direct payment offerings.

As the landscape shifts, the remaining MSPs are expected to shift their focus toward Business-to-Business (B2B) fleet solutions, which require alternative payment methods to avoid having the EV driver pay for charging individually. In this regard, MSP-issued RFID cards present a logical choice. However, there is also potential for credit card companies to offer solutions, such as creating debit cards exclusively for charging stations and possibly car wash services. This approach already exists for fuel stations and could be a viable alternative for charging stations too.

For this transition to credit card-based payments to be successful, strict adherence to the appropriate Merchant Category Code (MCC) will be necessary. Providing certain benefits to charging stations, like PIN pad exemption and potentially reduced transaction fees, could facilitate the adoption of credit card payments (e.g. through payment service directive - PSD2 facilitated by CPO lobby group(s)). Transportation and parking use cases already enjoy the strong customer authentication (SCA) exemption, as agreed upon in the Payment Services Directive, which is currently under review again. It remains to be seen if the PSD3 will contain new rules for the traditional MSP payment method. Why should credit cards need PIN and biometrics, but RFID cards do not?

These factors collectively suggest that credit cards could quickly become the most popular payment method in the charging ecosystem. A good example comes from the London Underground, where user behavior completely flipped after only four years of introducing credit card readers, surpassing the traditional Oyster card payment method. Although some Oyster card users, notably students and seniors, continue to enjoy reduced pricing, similar to how certain fleet use cases will persist for MSPs. This transformative shift was largely facilitated by the exemption of public transport from stringent customer authentication, such as PIN Pad requirements, as per the Payment Services Directive II EU regulation. For more details see: https://b2b.mastercard.com/reports/ev-charging-payments/

If MSPs really do wind up disappearing it will remain interesting to see who can replace them in terms of POI data collection and maintenance. Most likely, Google and Apple maps will step up to show the location, availability, and number of charge points per charger.

In summary, the pitch to new EV drivers will become more and more difficult. Even if a MSP product is included in the vehicle price for one year, simply getting new EV owners signed up will become an even greater challenge than it already is. Credit cards will work just fine like everywhere else.

To avoid going out of business, MSPs will have to adapt. They have a huge advantage in employing a large number of very smart E-mobility and charging experts, who are in high demand. In order to keep these employees, a path to growth and profitability must be on the roadmap. Here is a list of possible new business opportunities:

Embrace dynamic and site-specific pricing to apply advanced pricing strategies reflecting demand and CPO energy prices as main cost elements.

Drive the adoption of ISO 15118 Plug & Charge to stay relevant by providing enhanced customer experience

Regain focus on AC charging, where the credit card user journey with dynamic QR codes or central kiosks will be suboptimal and RFID cards are the better solution.

Consider offering a combined RFID and Credit Card for charging with loyalty program similar to collecting miles

Consider offering a credit card for fleets, which is restricted to charging and car care expenses

Transition to solutions for the Megawatt Charging Infrastructure for larger vehicles

Leverage expertise in charging activation, app and payments to offer White Label solutions to CPOs looking for their own app and direct payment solutions

Use existing data flow (CDRs) of real charging sessions to significantly improve POI data beyond what other specialists are able to do. Charge Detail Records, phone data and relationships with OEMs can verify GPS location, charging speed, opening hours and even find new stations from vehicle data. Use live data to recognize and anticipate expected waiting time at charging stations.

What do you think about the future of public charging payments?

Reply to this email, leave us a comment on the post online or join the discussion on LinkedIn.

This week’s newsletter is brought to you by Beehiiv.

We‘ve built Electric Avenue on beehiiv and the product velocity over the past year has been amazing. Beehiiv is simple enough to spin up your own newsletter in a day, but also offers advanced growth and analytics features for those that want to take it to the next level.

Check it out and start growing your own newsletter here.

3 Links 🔗

Going high voltage⚡: Industry rumors are circulating about Mercedes’ new EVA2M platform going up to 800V battery voltage. EVA2M will be a facelift of the EVA2 platform on which the EQE and EQS models are based.

Why this could be good news: It would allow Mercedes to go beyond the 200kW maximum charging power that they were previously limited to and keep up with other 800V-based cars.

Why this could be bad news: Mercedes just announced that their customers will gain access to Tesla’s Supercharger network in North America next year. As of today, Tesla’s network does not support battery voltages beyond 500V, so Mercedes is either banking on a Tesla retrofit campaign or they are spending $$ on a voltage booster for the EVA2M platform.

KIA x Wallbox ↔️ V2G: Korean automaker KIA and Spain-based charger manufacturer Wallbox announced this week that they’ll collaborate on DC V2G in North America. Starting in H1/2024, Wallbox’s Quasar 2 DC charger will be the first charger allowing bidirectional charging with KIA’s EV9 SUV. The Quasar 2 will support up to 11.5kW in DC bidirectional power flow, but no US pricing for the unit has been announced yet.

Ford CEO on charging anxiety & NACS: Check out this interesting 9min video interview by Ryan Levenson from TheKilowatts with Ford’s CEO Jim Farley.

Highlights:

Jim took a huge EV roadtrip and said “I don’t think I’ll ever use the range anxiety phrase again, because what I saw was charging anxiety”

Jim explained how the initial talks between Ford and Tesla about adoption of the NACS connector started, how they stalled - and how they got over the finish line.

Meme of the Week 🤡

That's a wrap for this week! Let us know how you feel (We read every single one of these reviews 🙂 ):

What do you think of today´s edition?

Reader Review of the Week

Selected ⚡️⚡️⚡️⚡️⚡️ Freakin´ awesome on ⚡ Mo Money, Mo Jobs: Policy Landscape Creates Electric Vehicle Jobs 💼 and wrote:

“Happy birthday electric Avenue!! One whole year of the best EV news I’ve gotten. Keep it up!"

Someone forwarded this to you? Subscribe now - it's free!

Looking to start your own newsletter? Sign up for Beehiiv now!

DISCLAIMER: None of this is financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. The Electric Avenue team may hold investments in or may otherwise be affiliated with the companies discussed.